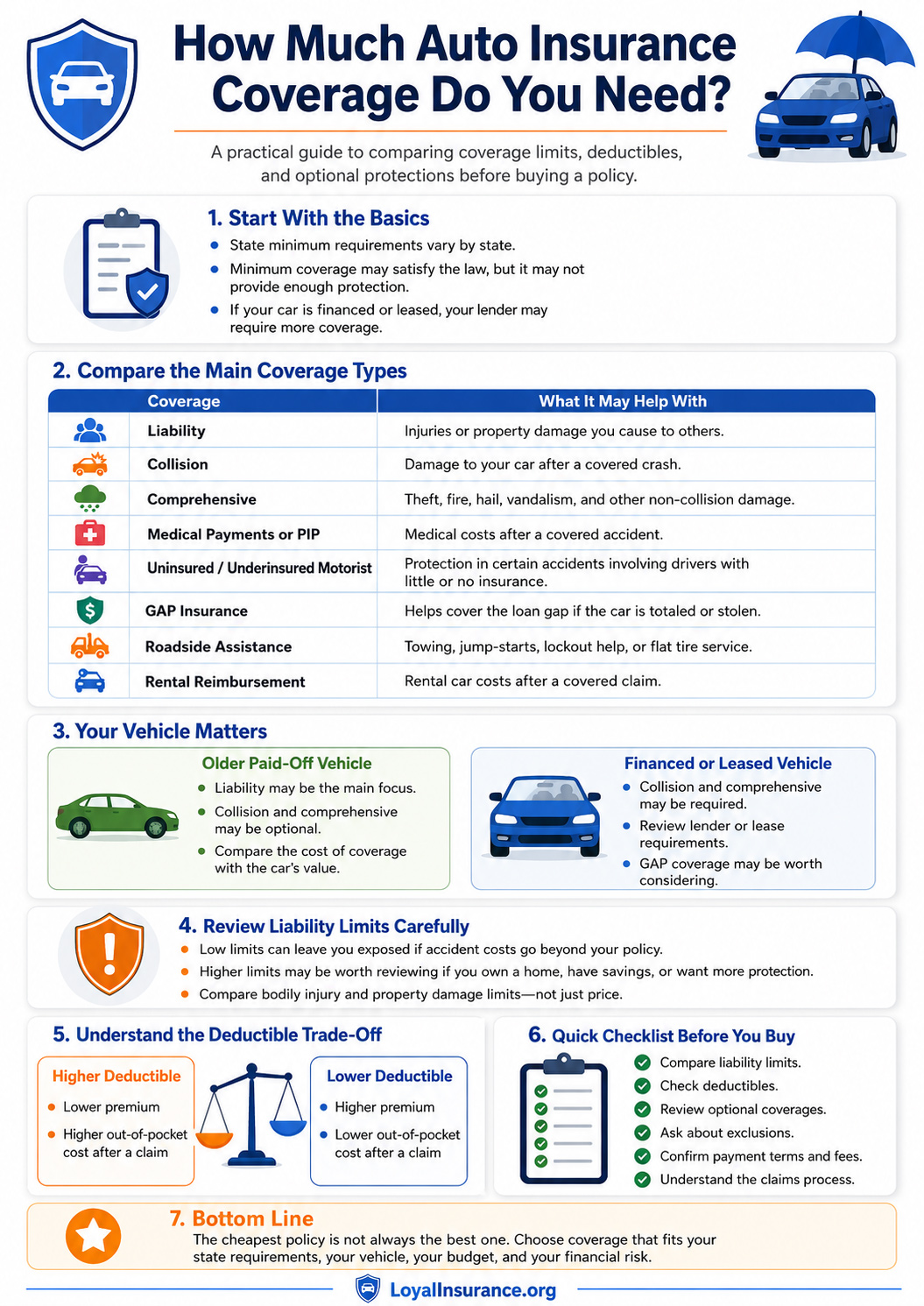

Finding a low auto insurance price can feel like the main goal, but the cheapest policy is not always the right policy. A good comparison should look at the monthly payment, the coverage limits, the deductible, the exclusions, the claims process, and whether the policy fits your state, lender, lease, vehicle, and household needs.

Most states require drivers to carry some form of auto insurance or financial responsibility before driving legally. The National Association of Insurance Commissioners explains that auto insurance commonly includes liability and property damage coverage areas, and state requirements can differ from one state to another.[1]

This guide explains how to think about auto insurance coverage before you compare quotes, including liability, collision, comprehensive, medical payments, uninsured motorist coverage, GAP insurance, towing, rental reimbursement, deductibles, and coverage limits.

Why the Cheapest Auto Insurance Quote May Not Be Enough

A low monthly payment can help your budget, but it does not automatically mean the policy gives you enough protection. Two quotes can look similar in price while offering very different liability limits, deductibles, optional coverages, payment fees, cancellation rules, and claims support.

The goal is not simply to buy the lowest-priced policy. The goal is to buy coverage that meets your legal requirements, protects you from realistic financial risks, satisfies lender or lease obligations when applicable, and still fits your budget.

Important coverage reminder: Before choosing a policy, compare what the policy pays for, what it excludes, how much the insurer may pay, how much you must pay out of pocket, and whether the coverage fits your vehicle and financial situation.

Start With State Minimum Requirements, But Do Not Stop There

Every driver should understand the minimum coverage required in their state. However, a state-minimum policy may only satisfy the legal baseline. It may not be enough to protect you financially after a serious accident, especially if damages exceed the selected liability limits.

The NAIC explains that liability limits are commonly shown as three numbers, such as 25/50/15. These numbers refer to the maximum amount the policy may pay for injuries to one person, injuries to all people in one accident, and property damage, subject to the policy terms.[2]

Questions to ask before choosing minimum coverage

- What are the exact bodily injury and property damage liability limits?

- What happens if accident costs exceed those limits?

- Does my state require uninsured motorist, underinsured motorist, PIP, or medical payments coverage?

- Does my lender or lease agreement require collision and comprehensive coverage?

- Can I afford the deductible if I need to file a claim?

- Are there exclusions, fees, or cancellation rules I should understand first?

Main Types of Auto Insurance Coverage to Compare

Auto insurance is made up of different coverage parts. Some may be required by state law, some may be required by a lender or lease company, and some may be optional. The Insurance Information Institute explains that common auto coverage types include liability, collision, comprehensive, medical payments, personal injury protection, uninsured motorist coverage, and other optional protections.[3]

| Coverage Type | What It May Help With | What to Compare |

|---|---|---|

| Liability coverage | May help pay for injuries or property damage to others when you are responsible for a covered accident. | Compare bodily injury limits, property damage limits, exclusions, and whether the limits are high enough for your risk level. |

| Collision coverage | May help pay for damage to your own vehicle after a covered collision, usually subject to a deductible. | Compare the deductible, vehicle value, loan or lease requirements, and whether the premium makes sense for the car. |

| Comprehensive coverage | May help with non-collision damage such as theft, fire, vandalism, weather, falling objects, or animal impacts, depending on the policy. | Compare covered events, deductible, exclusions, and whether the car’s value justifies the cost. |

| Medical payments or PIP | May help with medical costs after a covered accident, depending on the state and selected coverage. | Compare state rules, coverage limits, who is covered, and how the coverage coordinates with health insurance. |

| Uninsured or underinsured motorist coverage | May help in certain accidents involving a driver who has no insurance or not enough insurance. | Compare whether it is required or optional in your state, the available limits, and how claims are handled. |

| GAP insurance | May help cover the difference between what you owe on a loan or lease and what insurance pays if the car is totaled or stolen. | Compare loan balance, vehicle value, lender requirements, cost, cancellation rules, and whether you already have similar protection. |

| Towing and labor | May help with roadside support such as towing, jump-starts, flat tire service, or lockout help if included. | Compare service limits, distance limits, covered events, and whether you already have roadside assistance elsewhere. |

| Rental reimbursement | May help pay for a rental car if your vehicle is unavailable after a covered claim. | Compare daily limits, total maximum, when the benefit applies, and whether the coverage is worth the added cost. |

How Your Vehicle Affects the Coverage You May Need

The car you drive is one of the most important factors in choosing coverage. An older paid-off vehicle may not need the same protection as a newer financed vehicle. A car with a loan or lease may require collision and comprehensive coverage even if you would not otherwise choose those coverages.

The NAIC explains that if you have an auto loan, your lender may require full coverage, including comprehensive and collision coverage.[4] That means you should review your finance or lease agreement before dropping or changing coverage.

Older paid-off vehicle

- Liability coverage may be the legal minimum starting point.

- Collision and comprehensive may be optional if there is no lender.

- The car’s market value matters when deciding whether extra coverage is worth the premium.

- A higher deductible may reduce the premium but increases out-of-pocket cost after a claim.

Newer financed or leased vehicle

- The lender or lease company may require collision and comprehensive coverage.

- GAP insurance may matter if the loan balance is higher than the car’s value.

- Higher liability limits may be worth reviewing if you have more financial exposure.

- Rental reimbursement or roadside assistance may be useful depending on your situation.

How to Think About Liability Limits

Liability coverage is one of the most important parts of an auto insurance policy because it can help protect you when you are responsible for injuries or property damage to others in a covered accident. The higher your assets, income, savings, or financial exposure, the more important it becomes to review whether low liability limits are enough.

There is no single limit that is right for every driver. A person with very few assets, an older vehicle, and a tight budget may make different coverage decisions than a homeowner, business owner, high-income driver, or driver with a newer vehicle and significant loan or lease obligations.

When higher limits may be worth reviewing

- You own a home or have meaningful savings.

- You have a newer or financed vehicle.

- You regularly drive in high-traffic areas.

- You transport family members or other passengers often.

- You want more protection beyond the minimum required by law.

- You are concerned about being personally responsible for damages above your policy limits.

GAP Insurance for Financed or Leased Cars

Many drivers assume standard auto insurance will pay off the entire loan if a vehicle is totaled. That is not always how it works. Standard auto insurance generally pays based on the vehicle’s value, subject to the policy terms. If you owe more than the car is worth, you may still have a loan balance after the insurance payment.

The Consumer Financial Protection Bureau explains that GAP is an optional product intended to cover the difference between the amount owed on an auto loan and the amount the insurance company pays if the vehicle is stolen or totaled.[5]

Helpful example: If your car is worth less than your remaining loan balance, GAP coverage may help with the difference if the car is totaled or stolen and the coverage applies. Always review the cost, exclusions, cancellation rules, and whether the product is offered by your lender, dealer, insurer, or agent.

Deductibles Can Change the Real Cost of a Policy

The deductible is the amount you may need to pay out of pocket before certain coverage applies. A higher deductible can sometimes lower the premium, but it can also make a claim more expensive for you. A lower deductible may cost more each month but reduce the amount you owe after a covered claim.

When comparing quotes, do not only compare monthly payments. Compare the deductible, coverage limits, fees, and total policy cost. A cheaper policy with a much higher deductible may not be the better choice if you could not comfortably pay that deductible after an accident.

| Decision | Potential Benefit | Potential Trade-Off |

|---|---|---|

| Higher deductible | May reduce the premium. | You may pay more out of pocket after a covered claim. |

| Lower deductible | May reduce claim-time out-of-pocket cost. | The monthly or policy premium may be higher. |

| State-minimum liability | May satisfy legal requirements at a lower cost. | May leave you exposed if damages exceed the limits. |

| Higher liability limits | May provide more protection after a serious accident. | Usually costs more than minimum coverage. |

What to Compare Before Buying Auto Insurance

Before you choose a policy, compare the details that affect real protection. Monthly price matters, but it should not be the only factor. You should understand what the policy covers, what it does not cover, how claims work, what fees apply, and when coverage starts.

- Liability limits Review bodily injury and property damage limits, not just the monthly payment.

- Deductibles Confirm how much you would pay before collision or comprehensive coverage applies.

- Optional coverages Compare collision, comprehensive, rental reimbursement, roadside assistance, and GAP if relevant.

- Policy exclusions Ask what is not covered, especially for household drivers, business use, rideshare use, or excluded drivers.

- Payment terms Review down payment, monthly payment, installment fees, cancellation rules, and renewal terms.

- Claims process Confirm how to report a claim, what documents are needed, and how repairs or payments are handled.

Where Fred Loya Fits Into the Comparison

Some drivers include Fred Loya in their comparison because they want local office support, quick quote access, or a policy option focused on basic auto coverage. Before choosing any insurer, the better approach is to compare the actual policy details behind the price.

A Fred Loya quote may be useful as a starting point, but it should not be judged by the first payment alone. Review the liability limits, deductible, policy term, payment schedule, optional coverage, and whether the quote is still subject to verification.

Compare the policy, not just the brand name

Drivers looking at Fred Loya car insurance should check whether the quote includes only liability coverage or whether collision, comprehensive, roadside assistance, rental reimbursement, medical coverage, or uninsured motorist protection are also included.

A lower price may come from lower limits, fewer optional benefits, a higher deductible, or a shorter policy term. That does not automatically make the quote bad, but it does mean you should compare it against the same coverage structure from other insurers.

Questions to ask before choosing any insurer

- Is the quote final or still subject to verification?

- What liability limits and deductibles are included?

- Are collision and comprehensive included or excluded?

- Does the policy satisfy my lender or lease requirements?

- What discounts, fees, or payment charges apply?

- How do I get proof of insurance?

- How do I file a claim after an accident?

- What happens if I miss a payment or cancel the policy?

Use reviews and office access as secondary checks

A Fred Loya review can help you understand common customer concerns, service expectations, complaint themes, and coverage questions. Reviews should not replace the policy documents, but they can help you decide what to ask before buying.

Local support can also matter. Drivers who prefer in-person help may want to check nearby Fred Loya Insurance locations before choosing a policy, especially if they want help with payments, proof of insurance, policy changes, or coverage questions.

Comparison reminder: A good quote comparison uses the same vehicles, drivers, liability limits, deductibles, and optional coverages whenever possible. That makes it easier to see whether one policy is truly cheaper or simply offering less protection.

Questions to ask before choosing any insurer

- Is the quote final or still subject to verification?

- What coverage limits and deductibles are included?

- Are collision and comprehensive included or excluded?

- Does the policy satisfy my lender or lease requirements?

- What discounts, fees, or payment charges apply?

- How do I get proof of insurance?

- How do I file a claim?

- What happens if I miss a payment or cancel the policy?

Frequently Asked Questions About Auto Insurance Coverage

Is the cheapest car insurance policy always the best choice?

No. A cheaper policy may have lower limits, higher deductibles, fewer optional coverages, or stricter exclusions. The best choice depends on your state requirements, vehicle, lender or lease obligations, driving profile, budget, and financial risk.

How much liability coverage do I need?

There is no single answer for every driver. Start with your state minimum requirements, then consider your assets, income, savings, vehicle use, accident risk, and whether you want more protection than the legal minimum.

Do I need collision and comprehensive coverage?

You may need collision and comprehensive if your vehicle is financed or leased. If your car is paid off, these coverages may be optional, but they can still matter if you could not easily replace or repair the vehicle after damage or theft.

When does GAP insurance make sense?

GAP insurance may be worth reviewing if you owe more on your loan or lease than the vehicle is worth. It is most relevant when a vehicle is financed, leased, recently purchased, or depreciating faster than the loan balance is being paid down.

Should I raise my deductible to lower my premium?

A higher deductible may lower your premium, but it also means you may pay more out of pocket after a covered claim. Choose a deductible you could realistically afford if an accident happened.

Compare Auto Insurance Quotes by ZIP Code

Enter your ZIP code to continue comparing auto insurance quote options and review coverage details before choosing a policy.

Compare more than price. Review coverage limits, deductibles, policy terms, and quote details before choosing auto insurance.

Sources

This article was updated using official and consumer-focused insurance resources. Drivers should confirm final rates, policy terms, coverage availability, exclusions, discounts, fees, and eligibility directly with the insurer, agent, lender, or quote provider before buying coverage.

- National Association of Insurance Commissioners — Auto Insurance ↩

- National Association of Insurance Commissioners — Auto Insurance Shopping Tool ↩

- Insurance Information Institute — Auto Insurance Basics ↩

- National Association of Insurance Commissioners — What You Should Know About Auto Insurance Coverage ↩

- Consumer Financial Protection Bureau — GAP Insurance ↩