Fred Loya Insurance is often searched by drivers who want basic car insurance, local agency access, payment options, or help comparing coverage. This review explains what to know before choosing a policy, including coverage types, policy documents, claims considerations, and how to compare Fred Loya with other auto insurers.

This page is not an official Fred Loya website and does not sell insurance directly. It is an independent informational review designed to help drivers understand what to check before buying, renewing, or comparing an auto insurance policy.

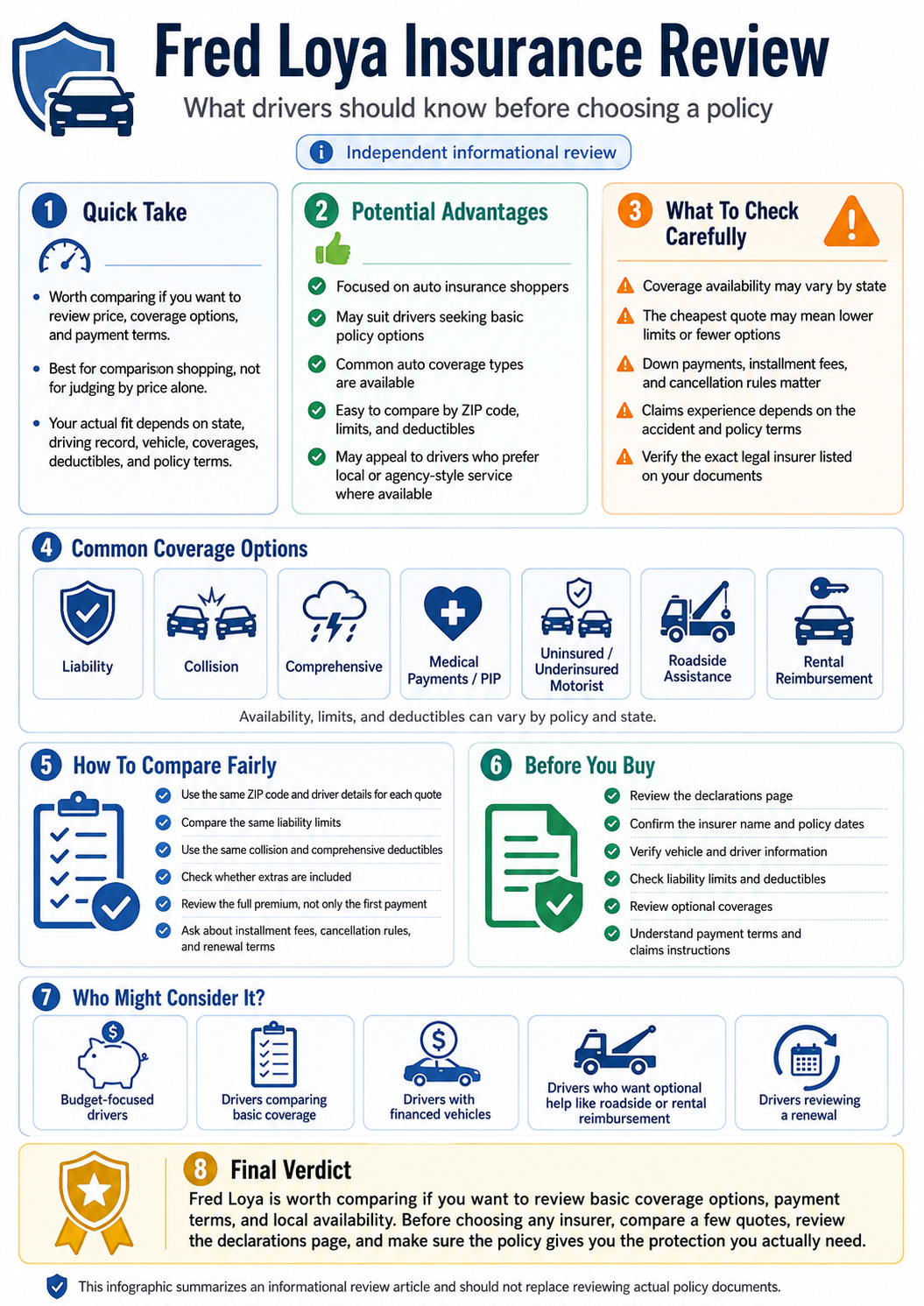

Fred Loya Insurance Review: What Drivers Should Know

A useful Fred Loya review should do more than say whether the company is “good” or “bad.” Auto insurance depends heavily on your state, driving record, vehicle, selected coverages, deductibles, payment plan, and claims history. A company that works for one driver may not be the right fit for another driver with different coverage needs.

Fred Loya’s official coverage information describes common car insurance options such as liability, comprehensive, collision, medical payments or personal injury protection, uninsured or underinsured motorist coverage, roadside assistance, and rental reimbursement.[1] However, availability, pricing, limits, and terms can vary, so the policy documents matter more than a general review.

Important coverage reminder: Do not choose an auto insurance policy based only on the monthly price or a company review. Review the declarations page, coverage limits, deductibles, excluded drivers, payment terms, cancellation rules, and claims instructions before buying.

Quick Review: Possible Pros and Cons

The strongest use of this page is to help you compare Fred Loya with other auto insurance options. The points below are general shopping considerations, not guarantees about your quote, claim, or final policy terms.

Potential advantages

- Focused on auto insurance shoppers.

- May appeal to drivers looking for basic policy options.

- Coverage pages explain common auto insurance terms.

- Can be compared with other insurers by ZIP code, limits, and deductibles.

- May be useful for drivers who prefer local or agency-style service where available.

Possible drawbacks to check

- Coverage availability may vary by state and location.

- The cheapest option may provide lower limits or fewer optional coverages.

- Installment fees, down payments, and cancellation rules can affect total cost.

- Claims experience can depend on the facts of the accident and policy terms.

- Drivers should verify the exact legal insurer listed on their documents.

What Coverage Does Fred Loya Offer?

Auto insurance is not one single product. A policy can include different coverage parts, each with its own limits, deductibles, exclusions, and state-specific rules. The NAIC explains that collision and comprehensive coverage are different from liability coverage and often come with deductibles.[2]

| Coverage Type | What It May Help With | What to Compare |

|---|---|---|

| Liability coverage | May help pay for injuries or property damage you cause to others in a covered accident. | Compare bodily injury limits, property damage limits, state minimums, and whether higher limits are available. |

| Collision coverage | May help pay for damage to your own car after a covered collision. | Review the deductible, vehicle value, lender or lease requirements, and exclusions. |

| Comprehensive coverage | May help with certain non-collision losses such as theft, hail, fire, vandalism, flood, falling objects, or animal impact, depending on the policy. | Check covered causes of loss, deductible amount, vehicle value, and policy exclusions. |

| Medical payments or PIP | May help with medical costs after an accident, depending on state rules and policy terms. | Ask whether it is required, optional, available, or excluded in your state. |

| Uninsured or underinsured motorist | May help when another driver has no insurance or not enough insurance, depending on the policy and state. | Confirm whether it is included, optional, required, rejected, or subject to separate limits. |

| Roadside or rental reimbursement | May help with towing, roadside help, or temporary transportation after a covered situation. | Check whether the option is included, added separately, limited by dollar amount, or subject to time restrictions. |

Is Fred Loya Good for Cheap Car Insurance?

Fred Loya may appear in searches from drivers looking for affordable auto insurance, but “cheap” does not always mean “best.” A lower premium can be helpful if it fits your budget, but it may also come with lower liability limits, higher deductibles, fewer optional coverages, or stricter payment rules.

Before deciding whether Fred Loya is a good option for you, compare the same coverage levels across multiple companies. For example, compare liability limits against liability limits, collision deductibles against collision deductibles, and monthly payment plans against the full policy cost.

How to compare fairly

- Use the same ZIP code and driver information for each quote.

- Compare the same liability limits when possible.

- Use the same collision and comprehensive deductibles.

- Check whether uninsured motorist, medical payments, roadside assistance, or rental reimbursement are included.

- Review the full premium, not only the first payment.

- Ask about installment fees, cancellation rules, and renewal terms.

Who Might Consider Fred Loya Insurance?

Fred Loya may be worth comparing if you are shopping for auto insurance and want to review basic coverage options, payment terms, and local availability. It may also be worth comparing if you want to see whether a policy can meet your state’s minimum requirements while still allowing you to add optional protection.

- Budget-focused drivers Compare the monthly cost, down payment, and total premium.

- Drivers comparing basic coverage Review liability limits and state requirements carefully.

- Drivers with financed vehicles Confirm whether collision and comprehensive are required by your lender.

- Drivers who want optional help Ask about roadside assistance, rental reimbursement, and medical payments.

- Drivers reviewing a renewal Compare the renewal premium with new quotes before accepting.

- Drivers with policy questions Check the declarations page, endorsements, and claims instructions.

What to Check Before Buying a Policy

The most important document in an auto policy is often the declarations page. This page usually summarizes the insured drivers, covered vehicles, policy period, coverage limits, deductibles, premium, lienholder, and selected options. A review online can help you ask better questions, but your policy documents control the actual coverage.

Policy details to verify

- The exact company or legal insurer name on the policy.

- The policy number, effective date, and expiration date.

- The vehicle year, make, model, and VIN.

- All listed drivers and any excluded drivers.

- Bodily injury and property damage liability limits.

- Collision and comprehensive deductibles if physical damage coverage is included.

- Medical payments, PIP, uninsured motorist, roadside, or rental options.

- Down payment, monthly payment, installment fees, and cancellation rules.

- Claim reporting instructions and required documentation.

Claims and Customer Experience: What to Know

Claims experience can vary from one accident to another. The outcome may depend on fault, coverage type, limits, deductibles, exclusions, documentation, state rules, repair estimates, and how quickly information is provided. This is why drivers should save photos, police reports, claim numbers, repair estimates, rental receipts, towing receipts, and all claim-related correspondence.

Before buying or renewing, ask how claims are reported, whether online or phone reporting is available, how inspections are handled, and what documents are needed after an accident. You can also use state insurance department resources and NAIC consumer tools to verify company information, complaints, licenses, and financial health.[3]

Practical tip: If your documents show a company name you do not recognize, confirm the insurer name through your policy paperwork, your agent, the insurer, or your state insurance department before relying on coverage.

How Fred Loya Compares With Other Auto Insurers

The best way to compare Fred Loya with another insurer is to compare the same coverage package side by side. A policy with a lower monthly price may not be better if it has lower limits, higher deductibles, fewer included coverages, or extra fees that raise the total cost over time.

Compare protection

- Liability limits

- Collision and comprehensive

- Medical payments or PIP

- Uninsured or underinsured motorist

- Roadside assistance

- Rental reimbursement

Compare total cost

- Full policy premium

- Down payment

- Monthly payment

- Installment fees

- Deductibles

- Cancellation or reinstatement rules

Final Verdict: Is Fred Loya Worth Comparing?

Fred Loya is worth comparing if you are shopping for auto insurance and want to review policy options, payment terms, and coverage availability. It may be especially relevant for drivers who are focused on price, basic coverage, or local agency access where available.

However, this review should not replace your own quote comparison. Before choosing Fred Loya or any other insurer, compare at least a few quotes, review the declarations page, check the legal insurer name, and make sure the policy gives you the protection you actually need.

Frequently Asked Questions About Fred Loya Insurance

Is Fred Loya Insurance a good company?

It depends on your needs, location, driving profile, coverage limits, payment plan, and expectations. Some drivers may consider Fred Loya when comparing affordable auto insurance options, but you should compare quotes, policy terms, claims instructions, and coverage details before buying.

Does Fred Loya offer full coverage?

“Full coverage” is not a single standard policy. Drivers often use the phrase to describe a policy with liability plus collision and comprehensive coverage, but the actual protection depends on the specific policy, limits, deductibles, exclusions, and state rules.

Does Fred Loya offer liability insurance?

Fred Loya’s coverage information describes liability coverage as part of its auto insurance coverage options. Liability coverage generally relates to covered injuries or property damage you cause to others, subject to limits and exclusions.

Should I choose Fred Loya only because the quote is cheaper?

No. A cheaper quote can help your budget, but you should also review limits, deductibles, optional coverages, fees, excluded drivers, cancellation rules, and claims instructions before choosing a policy.

How can I verify an insurance company?

You can check your policy documents, contact the insurer or agent, and use state insurance department resources. NAIC consumer tools can also help consumers find information about insurance company complaints, licenses, and financial health.

Compare Auto Insurance Quotes by ZIP Code

Enter your ZIP code to compare auto insurance quote options and review coverage details before choosing a policy.

Compare price, coverage limits, deductibles, fees, and policy terms before choosing auto insurance.

Sources

This article was updated using official company coverage information and consumer-focused insurance guidance. Drivers should confirm final rates, coverage availability, policy terms, discounts, fees, claims handling, and legal requirements directly with the insurer, agent, quote provider, or state insurance department before buying coverage.