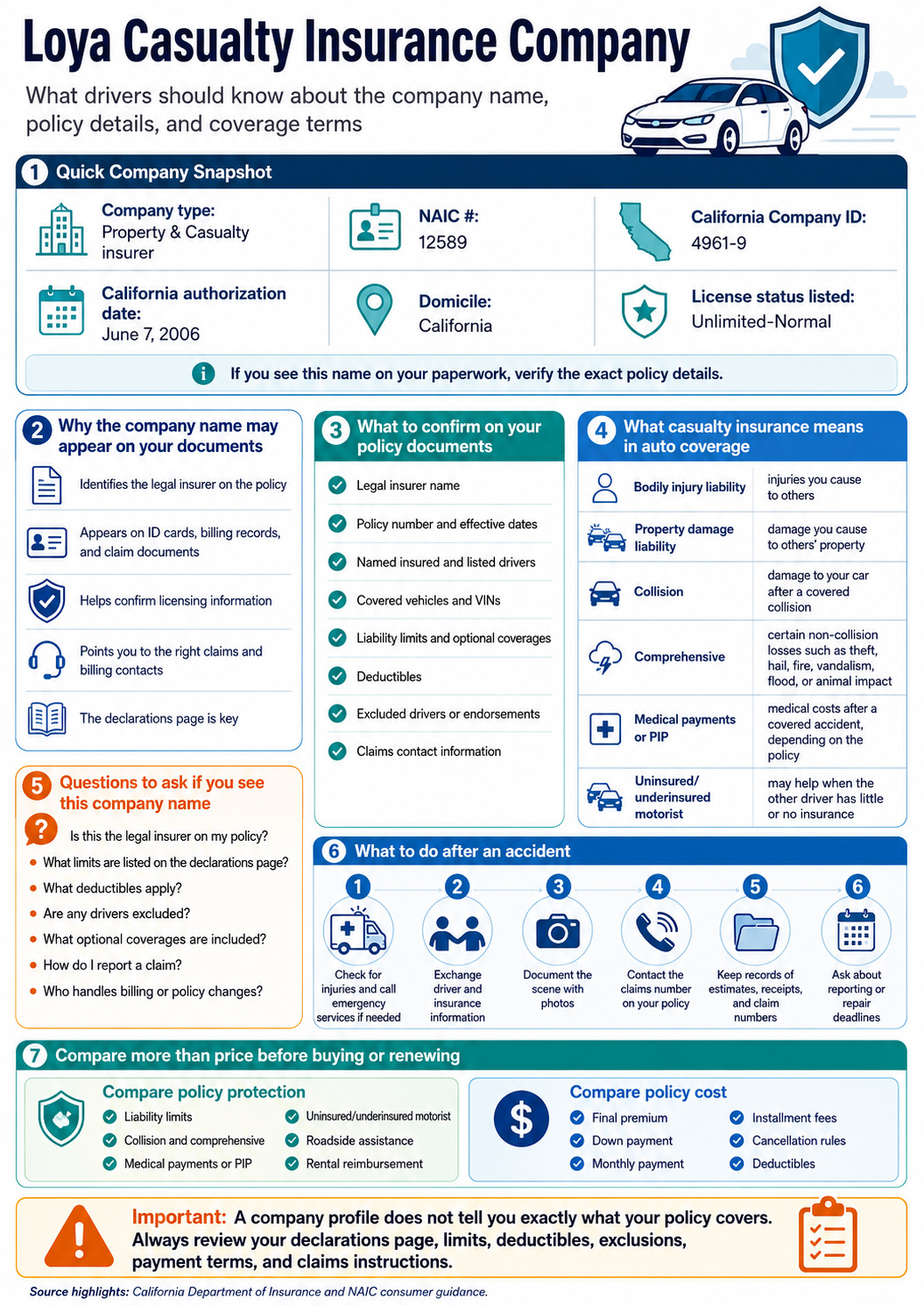

Loya Casualty Insurance Company is a property and casualty insurer listed by the California Department of Insurance. If you see this name on policy documents, insurance cards, billing records, claim documents, or company information, it is important to understand what the company name means and how to review the policy details connected to it.

The California Department of Insurance profile lists Loya Casualty Insurance Company with NAIC #12589, California Company ID #4961-9, a California authorization date of June 7, 2006, license status listed as unlimited-normal, company type listed as Property & Casualty, and state of domicile listed as California.[1]

This guide explains what drivers should know about the company profile, how casualty insurance relates to auto coverage, what coverage terms to review, and what questions to ask before choosing or renewing an auto policy.

What Is Loya Casualty Insurance Company?

Loya Casualty Insurance Company is not the same thing as a generic “coverage type.” It is the name of an insurance company. A company profile can matter because your policy, claim, declarations page, ID card, or billing record may show the legal insurer or related company responsible for the policy.

According to the California Department of Insurance, the company is authorized for lines of business including automobile, disability, and liability.[1] Drivers should still confirm the exact product, coverage, limits, fees, and claims process directly from their own policy documents or representative.

Important company reminder: A company profile does not tell you whether a specific policy is right for you. Always review the declarations page, limits, deductibles, exclusions, payment terms, effective date, and claims instructions before relying on coverage.

Why the Company Name May Appear on Your Documents

Auto insurance shoppers often focus on the brand name, local office, or quote platform. However, the legal insurer listed on the policy documents can be important. It may help you identify which company issued the policy, where to confirm license information, and which company may appear in claim or billing records.

If your paperwork shows Loya Casualty Insurance Company, check the declarations page carefully. The declarations page is usually where you can find the named insured, covered vehicle, policy period, coverage limits, deductibles, premium, lienholder information, and any listed drivers or excluded drivers.

Information to confirm on your policy documents

- Legal insurer name

- Policy number and effective dates

- Named insured and listed drivers

- Covered vehicles and VINs

- Liability limits and optional coverages

- Deductibles for physical damage coverage

- Excluded drivers, restrictions, or endorsements

- Claims contact information

California Licensing and Company Background

The California Department of Insurance company profile lists Loya Casualty Insurance Company as a California-domiciled property and casualty company with NAIC #12589.[1] The department’s 2022 examination report says the company was incorporated in California on December 14, 2004 and received its Certificate of Authority from the California Department of Insurance on June 7, 2006 to transact property and casualty business.[2]

The same examination report states that, as of December 31, 2022, the company was licensed to transact automobile insurance business only in California and wrote six-month policies for low limits of liability automobile insurance and low-value property damage automobile insurance through affiliates.[2]

Practical tip: If you are checking company information, use official state insurance department resources and your own policy documents. Do not rely only on old blog posts, third-party summaries, or search snippets for licensing or claims details.

What Casualty Insurance Means in Auto Coverage

In auto insurance, casualty-related coverage often connects to legal responsibility for injuries or property damage caused to others. For a driver, the most familiar example is liability coverage. Liability coverage is usually divided into bodily injury liability and property damage liability.

The NAIC explains that auto insurance coverage depends on the type of coverage chosen, and that many states require certain types of auto insurance. Its consumer guidance describes bodily injury liability, property damage liability, uninsured and underinsured motorist coverage, comprehensive coverage, collision coverage, medical payments, PIP, rental coverage, roadside coverage, and GAP insurance as separate concepts that may apply differently depending on state and policy terms.[3]

| Coverage Term | What It May Help With | What to Review |

|---|---|---|

| Bodily injury liability | May help pay for injuries you cause to someone else in a covered accident. | Review the per-person and per-accident limits, exclusions, and whether the limits are enough for your risk level. |

| Property damage liability | May help pay for damage you cause to another person’s vehicle, property, or structures. | Confirm the property damage limit and whether higher limits are available. |

| Collision coverage | May help pay for damage to your own vehicle after a covered collision. | Ask whether the coverage is included, optional, or required by your lender or lease company. |

| Comprehensive coverage | May help with non-collision losses such as theft, hail, fire, vandalism, flood, or animal impact, depending on the policy. | Review the deductible, exclusions, vehicle value, and covered causes of loss. |

| Medical payments or PIP | May help with medical costs after a covered accident, depending on the state and policy. | Confirm whether it is required, optional, available, or excluded in your state. |

| Uninsured or underinsured motorist | May help after certain accidents involving drivers with no insurance or not enough insurance. | Ask whether it is required, optional, included, or rejected in writing in your state. |

How This Page Differs From a General Loya Car Insurance Guide

This page focuses on the company profile and policy-document questions connected to Loya Casualty Insurance Company. If you want a broader overview of coverage, offices, quotes, payment options, and what to compare before buying, you can read our Loya car insurance guide.

For this page, the most important point is simple: the company name on your paperwork should lead you to verify the policy details, not assume what is covered. Two policies can come from similar brands or related companies but still have different limits, deductibles, exclusions, endorsements, fees, and claims instructions.

Questions to ask if you see this company name

- Is Loya Casualty Insurance Company the legal insurer on my policy?

- What is the policy number and effective date?

- What coverage limits are listed on the declarations page?

- What deductibles apply to collision or comprehensive coverage?

- Are any drivers excluded?

- Are roadside assistance, rental reimbursement, or medical payments included?

- How do I report a claim?

- Who should I contact for billing, cancellation, or policy changes?

What to Do After an Accident

If an accident happens, your first priority should be safety. Call emergency services if anyone is hurt or there is immediate danger. If it is safe and legal to do so, move vehicles out of traffic, exchange information, document the scene, and contact the claims number or instructions listed on your insurance documents.

Do not assume that every expense will be covered. Claim handling depends on the policy, coverage type, fault, limits, deductibles, exclusions, state rules, available documentation, and the specific facts of the accident.

- Check for injuries Call emergency services if anyone is injured or there is immediate danger.

- Exchange information Collect driver, vehicle, insurance, and contact details from the parties involved.

- Document the scene Take photos of vehicles, damage, road conditions, signs, and relevant surroundings if safe.

- Contact claims Use the claim instructions on your policy documents or insurer website.

- Keep records Save claim numbers, repair estimates, rental receipts, towing receipts, and correspondence.

- Ask about deadlines Confirm any reporting, inspection, document, or repair deadlines that may apply.

Coverage Details to Compare Before Buying or Renewing

Before buying or renewing any auto policy, compare more than the monthly price. A cheaper policy may have lower limits, higher deductibles, fewer optional coverages, stricter exclusions, or added payment fees. A more expensive policy may or may not provide enough extra value to justify the cost.

The NAIC advises drivers to understand what a policy covers, review required and optional coverage types, and compare policy terms carefully before buying auto insurance.[5]

Compare policy protection

- Liability limits

- Collision and comprehensive

- Medical payments or PIP

- Uninsured or underinsured motorist

- Roadside assistance

- Rental reimbursement

Compare policy cost

- Final premium

- Down payment

- Monthly payment

- Installment fees

- Cancellation rules

- Deductibles

Frequently Asked Questions About Loya Casualty Insurance Company

Is Loya Casualty Insurance Company an insurance company?

Yes. The California Department of Insurance lists Loya Casualty Insurance Company as a Property & Casualty company with NAIC #12589 and state of domicile listed as California.

What does NAIC #12589 mean?

An NAIC number is an identifier used for insurance companies in regulatory and company-reference contexts. If your documents list NAIC #12589, compare that information with the company profile and your policy paperwork.

Does the company profile tell me what my policy covers?

No. The company profile helps identify the insurer, but your actual coverage depends on your policy documents, declarations page, endorsements, limits, deductibles, exclusions, and state rules.

Is comprehensive coverage the same as collision coverage?

No. Collision coverage generally applies to damage from a covered collision, while comprehensive coverage generally applies to certain non-collision losses such as theft, hail, fire, vandalism, flood, or animal impact, depending on the policy.

Should I choose a policy only because the price is low?

No. Price matters, but you should also compare coverage limits, deductibles, exclusions, payment fees, claims process, and whether the policy satisfies your state, lender, or lease requirements.

Compare Auto Insurance Quotes by ZIP Code

Enter your ZIP code to compare auto insurance quote options and review coverage details before choosing a policy.

Compare price, coverage limits, deductibles, fees, and policy terms before choosing auto insurance.

Sources

This article was updated using official company-regulatory and consumer-focused insurance resources. Drivers should confirm final rates, policy terms, company information, coverage availability, discounts, fees, and legal requirements directly with the insurer, agent, state insurance department, or quote provider before buying coverage.

- California Department of Insurance — Loya Casualty Insurance Company Profile ↩ ↩ ↩

- California Department of Insurance — Loya Casualty Insurance Company 2022 Examination Report ↩ ↩

- National Association of Insurance Commissioners — What Does Auto Insurance Cover? ↩

- Fred Loya Insurance — Car Insurance Coverage

- National Association of Insurance Commissioners — Auto Insurance Consumer Information ↩